What Rising Interest Rates Mean for Business

Some interest rates have begun to rise, with others certain to follow. The Federal Reserve has stated its plan to stop buying long-term securities and start pushing short-term interest rates up in March 2022. What this means for business varies, but it’s mostly not good. The alternative, though, would be higher inflation—very definitely not good.

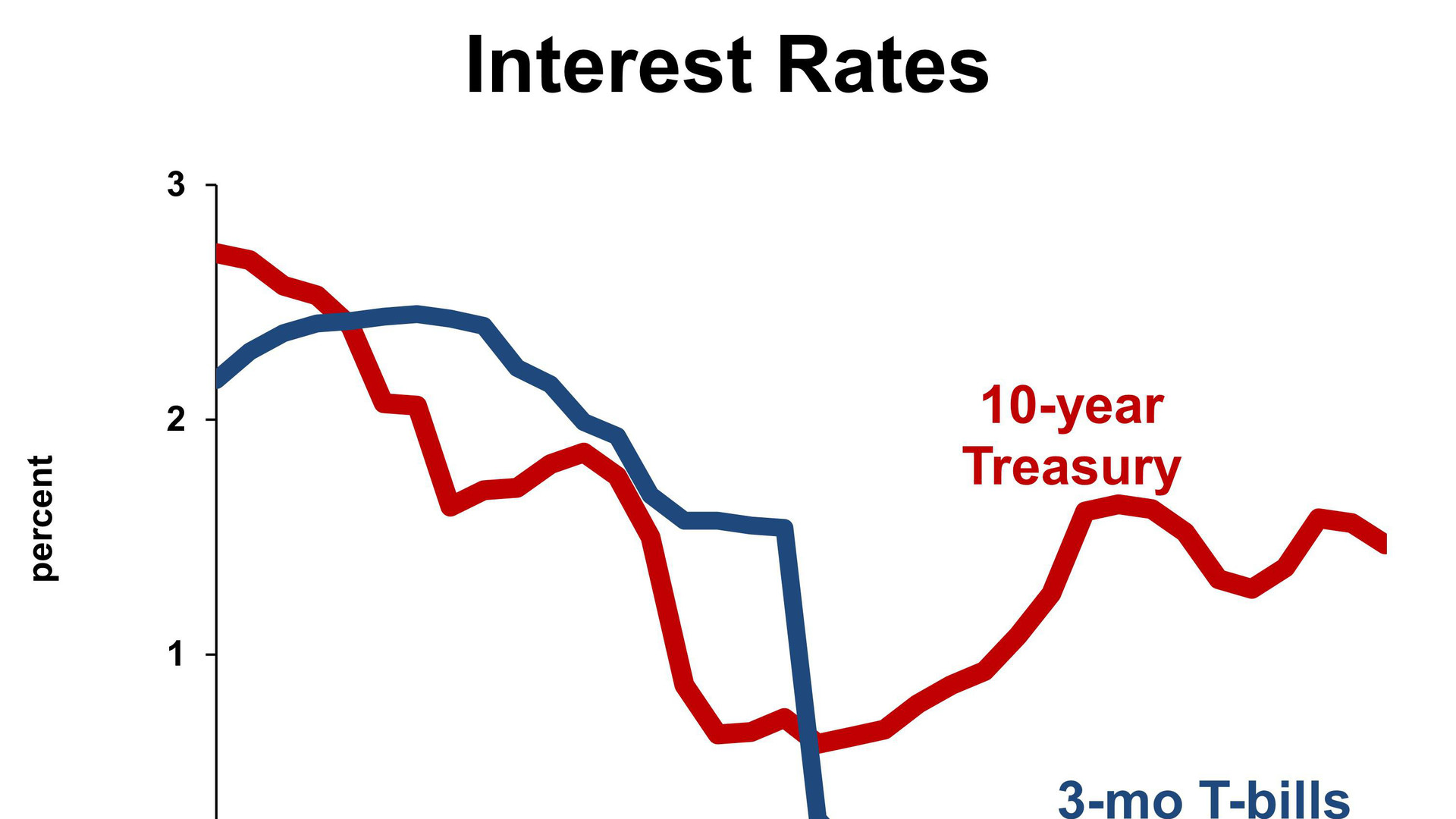

The increase in long-term interest rates has been driven by global economic recovery, which led to an increase in global demand for credit relative to global savings. Added to that is U.S. inflation, which pushes our long-term interest rates up relative to lower-inflation countries.

Short-term interest rates will be pushed up by the Federal Reserve, as the Fed announced. They will raise rates in quarter-point increments three or four times this year. They will still be behind the curve, most likely, and will raise short rates more aggressively in 2023.

Looking first at business revenue, companies with extra cash will earn a little bit more interest as the Fed raises short-term interest rates, but this will hardly be significant for most companies.

On the revenue downside, interest-sensitive businesses will see less demand for their goods and service. The mortgage industry will find fewer homeowners refinancing their mortgages. The demand for houses, though, is probably strong enough that higher mortgage costs will have only a small effect, and that will impact pricing more than the number of new homes built and sold.

Cars and some capital equipment are also interest-sensitive, but pent-up demand is quite strong. Again, volume will probably be fine at first, but aggressive pricing won’t work as well for manufacturers of such products. Non-residential construction will also be affected, but interest rates are starting out at such a low level that another percentage point won’t do much to stop projects that make a lot of sense today.

On the expense side of the ledger, companies will see higher borrowing costs for both operating lines and term loans. Many business lines reprice monthly, so higher interest expense hits the company immediately. Term loans are common for real estate, such as owner-occupied buildings, and they will only reprice over time.

After the initial business impacts, focused on interest-sensitive sectors, ripple effects will spread across the economy. Companies that are not particularly interest-sensitive will see lighter sales growth because of generally slower economic expansion. If the Fed fails to tighten at exactly the right time, in exactly the right magnitude, with exactly the right end of its tightening, then recession will ensue. As of this writing, recession appears several years away.

Business strategy should first recognize specific impacts to the business of higher interest rates, then look at the possibility of a serious recession in later years. These good times can be used to lay the foundation for surviving the next downturn in the economy, which will be brought on by the Fed’s tightening.

This article was written by Bill Conerly from Forbes and was legally licensed through the Industry Dive Content Marketplace. Please direct all licensing questions to legal@industrydive.com.